The Impact of the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA) on Combating Cryptocurrency-Related Fraud and Money Laundering in Canada

Introduction

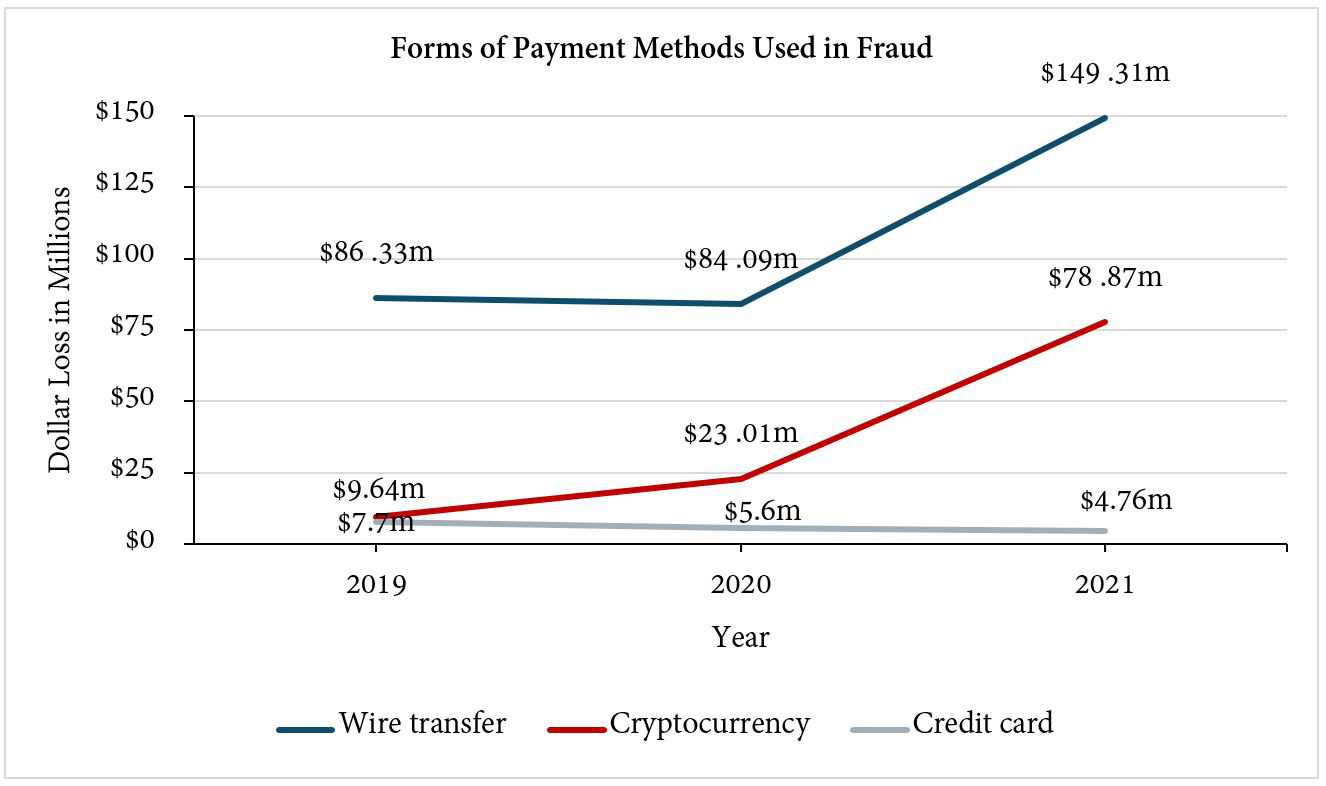

According to a survey conducted by the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) in 2021, money laundering transactions amounted to approximately $2.88 billion (FINTRAC, 2022). The survey included municipal, provincial, and federal law enforcement agencies. In the Greater Toronto Area, a 15-month investigation into organized crime resulted in the seizure of $370,000 and an undisclosed "large" number of cryptocurrency. Additionally, 114 financial service businesses had their registrations with FINTRAC revoked due to non-compliance with the PCMLTFA (Proceeds of Crime (Money Laundering) and Terrorist Financing Act). Interest in cryptocurrency has continued to grow, with Canada witnessing a significant 238% increase in cryptocurrency fraud from 2020 to 2021 (CAFC, 2021). In 2022, $308.6 million was lost from cryptocurrency investment fraud (Competition Bureau, 2023). According to the CAFC, cryptocurrency investment fraud has emerged as the most expensive type of fraud. In 2021, there were 3,442 cases of investment fraud, leading to losses of nearly $164 million (CAFC, 2021). Of this amount, cryptocurrency accounted for $77 million (Figure 1). On average, each report accounted for a loss of approximately $47,625. Seniors aged 60 years and older were particularly vulnerable, experiencing a collective loss of $38 million across 487 reports, equating to an average loss of $78,000 per report.

These alarming statistics indicate a growing trend in the detection of cryptocurrency-related fraud. It is important to note that the reported cases of fraud involving Canadian victims represent only a small portion, estimated to be between 5% and 10%, of the total fraudulent activities that occur (CAFC, 2021). This implies that there are more unreported crimes occurring under the radar. However, it is possible that cryptocurrency fraud is becoming more well-known because of the policy and are being reported more than before. The PCMLTFA has achieved some successes in establishing clear standards and adhering to international best practices. However, it has faced challenges in keeping pace with the rapidly evolving cryptocurrency industry.

Figure 1. The top 3 forms of payment methods used in fraud in Canada. These methods include wire transfer, cryptocurrency, and credit card transactions.

The Objectives of the PCMLTFA

The most important formal decision in this case is the amendment of the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (PCMLTFA) in 2019 by the Canadian government. The amendment to the PCMLTFA aimed to regulate cryptocurrency in order to fulfill Canada's international commitments in combating transnational crime, particularly money laundering and terrorist activity. Its objective was to facilitate the international fight against illicit financial activities and ensure the integrity of the financial system (PCMLTFA, 2000, c. C-17). According to the Proceeds of Crime (Money Laundering) and Terrorist Financing Act (2000, c. C-17), the objectives were “to facilitate combatting the laundering of proceeds of crime and combatting the financing of terrorist activities, to establish the Financial Transactions and Reports Analysis Centre of Canada and to amend and repeal certain Acts in consequence”. To achieve these objectives, the PCMLTFA implemented measures to detect and deter money laundering and the financing of terrorist activities, while also using various policy instruments to protect the financial system and fulfill international commitments in the fight against cryptocurrency-related crimes.

Policy Instruments of the PCMLTFA for Addressing Money Laundering and Terrorist Financing in Cryptocurrency Transactions

The PCMLTFA outlined specific legal measures for financial service providers and investors, including regulations for record keeping, client identification, reporting, and enforcement (PCMLTFA, 2000, c. C-17). It also established FINTRAC as the organization responsible for overseeing compliance and handling information related to money laundering and terrorist financing in relation to cryptocurrency transactions. The policy instruments used in the implementation of the PCMLTFA were comprehensive and designed to address money laundering and the financing of terrorist activities. Noncompliance with the policy instruments could result in severe penalties, including fines of up to $500,000, as well as potential imprisonment for a maximum of five years. These policy instruments worked together to detect and deter money laundering and the financing of terrorist activities, facilitate the investigation and prosecution of related offenses, fulfill international commitments, and protect Canada's financial system.

Policy instruments for addressing money laundering and terrorist financing in cryptocurrency transactions:

Record keeping and client identification requirements: Financial service providers and individuals involved in businesses at risk of money laundering or terrorist financing must maintain client records, verify client identities, and keep transaction records (PCMLTFA, 2000, c. C-17). These requirements enhance transparency and traceability, making it difficult for criminals to conceal their illicit activities.

Reporting of suspicious financial transactions and cross-border movements: The PCMLTFA mandated the reporting of suspicious financial transactions and international movements of currency and monetary instruments. When there were suspicions of money laundering, fraud, or terrorist financing, authorities had to be notified. This instrument enabled early detection and intervention to mitigate illegal activities. However, it was important to adjust this instrument in order to prevent money laundering and terrorist financing. Recent research has shown that suspending suspicious accounts was essential in addressing global financial crimes (Kirimhan, 2022). While transactions of $10,000 or more were already required to be reported to FINTRAC, the PCMLTFA should have also mandated financial service providers to temporarily suspend accounts involved in suspicious activities, in addition to reporting them to FINTRAC.

Establishment of an agency: The PCMLTFA established the Financial Transactions and Reports Analysis Centre of Canada (FINTRAC) as the key agency responsible for overseeing policy implementation. FINTRAC assesses reports and ensures that financial service providers comply with the policy.

Exchange of necessary information with law enforcement officials: This instrument facilitated the exchange of information between intelligence agencies, such as CSIS, and law enforcement agencies, such as the RCMP, to support investigations related to financial crimes. It facilitated the detection and prevention of criminal offences in the cryptocurrency sector.

Fulfillment of international commitments: The PCMLTFA implemented measures aligned with international standards, demonstrating Canada's commitment to combating global money laundering and terrorist financing. This included cooperation with international bodies such as the Financial Action Task Force (FATF). Cryptocurrency-related criminal activity has transnational implications, necessitating coordination and cooperation at the international level. Canada's enactment of this legislation exemplified its dedication to combating transnational crime on a global scale. The country actively collaborated with other nations and international organizations to foster information sharing, coordinate enforcement actions, and implement effective measures that followed the international standards in the fight against money laundering and terrorist financing.

Protection of the financial system: The PCMLTFA aimed to safeguard Canada's financial system from exploitation for money laundering and terrorist financing. This involved implementing regulations, supervisory frameworks, and risk-based approaches to identify, assess, and mitigate the risks associated with illicit financial activities. For example, financial institutions and other entities at risk of money laundering or terrorist financing were required to assess the risk of such activities and establish policies and procedures accordingly. If the risk was deemed significant or under specific circumstances, they were to take additional measures, such as conducting due diligence, continuously monitoring business relationships, and promptly reporting suspicious transactions to FINTRAC. These additional measures included conducting thorough due diligence, continuously monitoring the business relationship, and promptly reporting any suspicious transactions to FINTRAC. Through these measures, Canada strives to maintain the integrity and stability of its financial system.

Multilevel Governance in the Implementation of the PCMLTFA

The case of the PCMLTFA illustrates the concept of multilevel governance, which involves coordination among the subnational actors, central government, and international entities (Schakel, 2016). At the national level, the Canadian government took the initiative to amend the PCMLTFA in order to regulate cryptocurrency and address concerns related to money laundering and fraud (PCMLTFA, 2000, c. C-17). This decision demonstrated the authority of the central government in setting policy objectives and designing the necessary instruments. Subnational actors, including cryptocurrency exchanges and FINTRAC, were then responsible for implementing and enforcing the policy. Furthermore, the policy intersected with international governance due to the transnational nature of cryptocurrency transactions, requiring coordination and cooperation on an international scale. The Canadian government's decision to regulate cryptocurrency aligned with broader international efforts, such as those led by the FATF, to combat global money laundering and terrorist financing.

Vertical Relations of Authority and Multilevel Governance in the PCMLTFA

The PCMLTFA did not decentralize authority to local governments (Schakel, 2016). While there was coordination and cooperation between the federal government and other stakeholders, the implementation of the policy remained under the control of the federal government (PCMLTFA, 2000, c. C-17). Additionally, the PCMLTFA operates at various levels, involving different stakeholders and bodies of government. At the federal level, the Canadian government holds the highest authority in implementing and the PCMLTFA. The executive branch, under the leadership of the Prime Minister and the cabinet, formulates policies and oversees their implementation. The legislative branch, consisting of the Senate and the House of Commons, engages in discussions and can either approve or refuse these policies. Therefore, the federal government regulates and enforces measures against money laundering and terrorist financing throughout the nation.

There was also coordination between the federal government and other stakeholders at lower levels of authority. Financial institutions, such as the Bank of Canada, were involved in implementing and enforcing the policies, as they had a high interest and power in maintaining monetary sovereignty (FINTRAC, 2022). Cryptocurrency exchanges also played a role by monitoring cryptocurrency transactions and complying with the new regulations. Law enforcement agencies, including the RCMP and FINTRAC, worked closely with the government in researching cryptocurrency-related offenses (Posadzki, 2014).

Sabatier’s implementation framework

Sabatier's implementation framework is a structured and comprehensive approach to policy implementation. It encompasses six elements, including policy design, target groups, and behavior modification, which are used to measure the success of policy implementation (Sabatier, 1986). The target group identified in the policy design of the PCMLTFA includes individuals and businesses engaged in cryptocurrency. The behavior to be modified by the policy pertains to accurately recording transactions and reporting suspicious transactions to promote transparency and accountability in the cryptocurrency sector.

Evaluation of the PCMLTFA in Sabatier's Implementation Framework

Clear, consistent objectives:

The PCMLTFA established clear objectives in its provisions and included specific regulatory requirements. For example, it mandated the reporting of transactions of $10,000 or more to FINTRAC and mandated customer due diligence (PCMLTFA, 2000, c. C-17). The PCMLTFA also provided a framework for detecting and deterring criminal activity.

Adequate causal theory:

The PCMLTFA was based on the belief that imposing regulatory obligations on reporting entities, financial institutions, and cryptocurrency exchanges would disrupt the ability of criminals to launder money and finance terrorist activities (PCMLTFA, 2000, c. C-17). It was grounded in the assumption that increased transparency, due diligence, and reporting of suspicious transactions would contribute to the identification and prevention of money laundering and terrorist financing. Therefore, the PCMLTFA had an adequate causal theory, as it provided a structured rationale for how the policy would achieve its intended effects by identifying the cause and effects of the policy interventions and the resulting social outcomes.

Legal structuring:

The PCMLTFA, as a comprehensive legislative framework, involved the structuring of legal provisions related to anti-money laundering and counter-terrorist financing measures. The framework had adequate legal structure that aligned with the PCMLTFA's objectives of establishing legal requirements for record keeping and reporting entities (PCMLTFA, 2000, c. C-17).

Committed, skillful implementing officials:

The director of FINTRAC, as mandated by the PCMLTFA, had to have extensive knowledge and expertise in financial analysis, terrorist financing, and money laundering (PCMLTFA, 2000, c. C-17). This requirement ensured that the director was fully equipped to implement the provisions of the PCMLTFA related to money laundering and terrorist financing. The requirement for the director to have an advanced understanding and experience in these areas facilitated the effective execution of the policy.

Supportive interest groups, sovereigns:

The RCMP played an active role in developing policy recommendations and researching cryptocurrencies and their potential for money laundering (Posadzki, 2014). Their ongoing investigations into cryptocurrency-related crimes were instrumental in amending the PCMLTFA. Financial institutions and law enforcement agencies, including the RCMP, the Bank of Canada, and FINTRAC, provided support for the amendment. Additionally, the PCMLTFA received strong political support from both the legislative and executive branches of the Canadian government, as it was passed with the support of the Senate and the House of Commons.

Supportive socio-economic conditions:

The socio-economic conditions were not ideal for the implementation of the policy. The COVID-19 pandemic had a significant impact on the Canadian economy, including its anti-money laundering and anti-terrorist financing measures. The pandemic created new challenges and risks for financial institutions and cryptocurrency exchanges subject to the PCMLTFA. Criminals exploited the economic disruption and uncertainty caused by the pandemic to carry out money laundering operations and fraudulent activities (FATF, 2020). For instance, criminals used fraudulent schemes related to COVID-19, such as the sale of fake medical equipment or the exploitation of government relief programs, to launder money. Additionally, criminals capitalized on the pandemic to finance terrorist activities. During the pandemic, the disruption of supply chains was leveraged by the criminals to smuggle weapons and used the pandemic to fundraise illicit activities.

The pandemic presented new challenges for financial institutions and other entities subject to the PCMLTFA, and had to adjust to the challenges associated with remote work and digital transactions (FATF, 2020). During the pandemic, many financial institutions had to develop new strategies for assessing and mitigating risks associated with the growing use of virtual currencies and online payment systems. This was necessary to mitigate the increasing incidents of money laundering operations and terrorist financing offences. Therefore, it is necessary for the PCMLTFA to provide up-to-date best standards in anti-money laundering policies for financial institutions and cryptocurrency exchanges to adhere to.

Cryptomarkets and Non-Fungible Tokens: Emerging Risks in Money Laundering

Research has found that the use of cryptomarkets, or e-commerce platforms on the dark web, has become increasingly popular among organized crime groups (Kabra & Gori, 2023). This is because tracing the origin of funds is difficult, enabling these groups to evade law enforcement agencies. To launder cryptocurrencies, organized crime groups use a complex chain of transactions involving multiple accounts and locations. This movement of funds disguises their illicit nature, making it challenging to identify them as proceeds from drug trafficking.

Furthermore, non-fungible tokens (NFTs), which are closely related to the cryptocurrency market, are increasingly recognized as a risk for money laundering (Mosna & Soana, 2023). NFTs are unique digital assets that act as collectible art pieces and can have subjective prices. For instance, "The Merge," an NFT created by the artist Pak, was sold to a collective of 28,983 buyers for a total of $91.8 million (Block, 2021). This emphasizes the significant potential for money laundering, as NFTs function similarly to traditional art but require the use of cryptocurrencies for acquisition. The subjective pricing of NFTs also allows malicious actors to manipulate prices and launder illicit funds (Mosna & Soana, 2023). Additionally, the absence of customer due diligence checks on NFT sales platforms further facilitates such activities. Given the increasing sophistication of money laundering techniques, it is crucial for the PCMLTFA to adapt to emerging blockchain technologies in order to effectively combat financial crimes.

Conclusion

The PCMLTFA has achieved success in setting clear and consistent objectives to combat money laundering and terrorist financing. It has also shown a commitment to fulfilling international obligations in the fight against global financial crimes. The PCMLTFA outlines specific legal measures, including record-keeping requirements, reporting of suspicious transactions, and the establishment of FINTRAC as the primary implementing organization. These measures help improve transparency in cryptocurrency transactions compared to before when the policy wasn’t in place.

However, the implementation of the PCMLTFA is an ongoing process that requires continuous evaluation and adaptation to emerging challenges. For instance, the COVID-19 pandemic has created new opportunities for organized crime, highlighting the need to adjust policies and measures to address these evolving threats. Strengthening the PCMLTFA by incorporating measures such as temporary account suspensions for suspicious activities, and addressing the risks associated with cryptomarkets and NFTs, can further enhance its effectiveness in combating money laundering and terrorist financing. Ongoing evaluation, adaptation, and collaboration among stakeholders are crucial in the ever-evolving landscape of cryptocurrency.

References

Block, F. (December 7, 2021). PAK’s NFT Artwork ‘The Merge’ Sells for $91.8 Million. Barrons. Link

CAFC (2022). Canadian Anti-Fraud Centre Annual Report 2021. Government of Canada. Link

Competition Bureau Canada (2023). Quick easy money? Sometimes it’s a quick easy LIE. Link

Fletcher, E., Larkin, C., & Corbet, S. (2021). Countering money laundering and terrorist financing: A case for bitcoin regulation. Research in International Business and Finance. Link

Financial Action Task Force (FATF). (2020). COVID-19-related Money Laundering and Terrorist Financing – Risks and Policy Responses. Paris, France. Link

Kabra, S., & Gori, S. (2023). Drug trafficking on cryptomarkets and the role of organized crime groups. Journal of Economic Criminology. Link

Kirimhan, D. (2022). Importance of anti-money laundering regulations among prosumers for a cybersecure decentralized finance. Journal of Business Research. Link

Mosna, A., & Soana, G. (2023). NFTs and the virtual yet concrete art of money laundering. Computer Law and Security Review. Link

Proceeds of Crime (Money Laundering) and Terrorist Financing Act (2000, c. C-17). Link

Sabatier, P. A. (1986). Top-down and bottom-up approaches to implementation research: A critical analysis and suggested synthesis. Journal of Public Policy, 6(1), 21–48. Link

Schakel, A. H. (2016). Applying multilevel governance. In H. Keman & J. Woldendorp (Eds.), Handbook of Research Methods and Applications in Political Science (pp. 97-110). Cheltenham: Edgar Elgar. Link

Schakel, A. H. (2016). Exploring and explaining trends in decentralization. In H. Keman & J. Woldendorp (Eds.), Handbook of Research Methods and Applications in Political Science (pp. 97-110). Cheltenham: Edgar Elgar. Link

Posadzki, A. (2014, September 10). RCMP studying Bitcoin to help solve crimes, emails show. Global News. Link